January 2015 – Automatic enrolment

-

January 2015: Automatic enrolment

In January 2015, the government announced that 5 million people had been enrolled into a workplace pension. -

February 2015: Get your State Pension statement

In February 2015 the government extended the age that you can get a State Pension statement, meaning people aged 55 and over can find out their entitlement. Click here to find out how to get your statement... -

April 2015: Pension freedoms and Pension Wise

From 6th April 2015 people who retire will have more choices for how to use their pension pots, and the free guidance service Pension Wise will go live. Click here to find out more... -

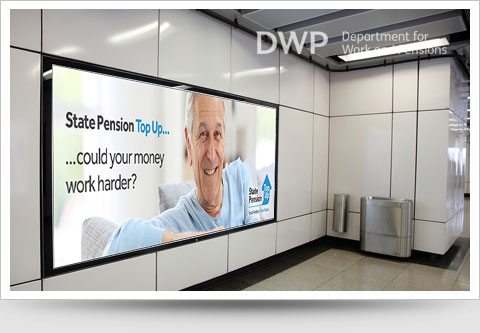

October 2015: State Pension top up

From 12th October 2015 people who are already retired will be able to 'top up' their State Pension by up to £25 a week, through this new government scheme. Click here to find out more... -

April 2016: State Pension changes

The State Pension is changing on 6th April 2016, meaning that everyone who retires after that date will get the new State Pension. Click here to find out more...

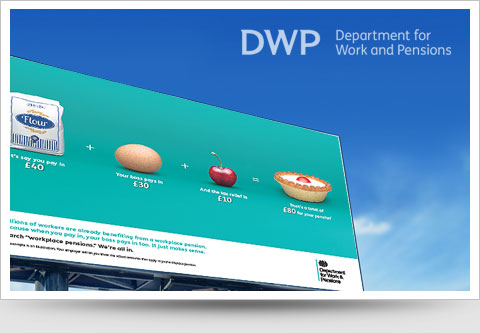

Back in 2012, only 1 in 3 people were saving into a workplace pension, meaning that most wouldn’t have enough to fund their retirement. So the government decided to ‘automatically enrol’ them into a workplace pension.

This means that you contribute a small percentage of your pay, your employer pays in too, and the government gives you tax relief—meaning that you get a bigger pension pot than if you went it alone. We like to think of the equation a bit like this…

![]()

Auto-enrolment applies to everyone aged over 22, who is in work and earns over £10,000 a year. So the likelihood is that you have been or will be auto-enrolled. And seeing as 9 out of 10 people stay enrolled in their workplace pension, you probably stayed in too. Good choice!

If you want to see what sort of retirement your pension could get you – take a look at this video! [Meet Derek the ultimate #PensionFan]

If you want more information about auto-enrolment:

Visit www.gov.uk/workplacepensions

Visit www.youtube.com/pensiontube

Or ask your employer.

| Myth I’m relying on my partner or I’ll inherit money from my parents |

Busted Inheritances can be uncertain and as people live longer you may have to wait longer for money you’ll be relying on. Your parents could still be alive when you retire. You need to make your own pension arrangements. |

| Myth It’s not worth saving into a pension |

Busted Oh yes it is. We all know that pension savings can go down as well as up. But analysis of the industry shows 95 per cent of people can expect to get back more during their retirement than they put in |

| Myth My house will be my pension pot |

Busted Be wary because property doesn’t allow you to spread your money across a range of different investments in the way saving into a pension does. And you don’t have the same tax advantages or contributions from your boss. |

| Myth I can only pay a small amount so it’s not worth it |

Busted Your contributions may be a small percentage of your salary but you will also benefit from extra money with contributions from your boss and through tax relief. Saving regularly and starting as early as possible will enable you to build up a pot to help give you a more secure financial future. |

| Myth I’ve left it too late to start saving |

Busted It’s never too late to start making contributions. Better late than never. And if you don’t you’ll be turning down extra money from your employer and tax relief. |

| Myth My grandma only lived to 70, I won’t live much longer. Why bother? |

Busted People tend to underestimate how long they are going to live and life expectancy keeps rising. We are likely to spend an average 20 years in retirement, so you do need to put something away for that. |

Have you been auto-enrolled? Did you stay in or opt-out? Let us know in the comments.